The bisphenol A industry breaks multiple constraints and requires multipolarization

February 09, 2022

After the bisphenol A market in China experienced a series of shocks in 2007, the price dropped to below 16,000 yuan/ton. The price of BPA eventually failed to return to a more reasonable range in the context of rising international oil prices and raw material phenol and ketone prices. Although there is still a significant increase compared to the level of less than RMB 11,000/ton at the beginning of 2006, it is obviously unsatisfactory from the perspective of input and output due to the increase in the cost of raw materials phenol ketone. Looking ahead, the development of domestic bisphenol A industry is facing multiple constraints, and it is urgent for multiple parties to make joint efforts to break through the bottleneck.

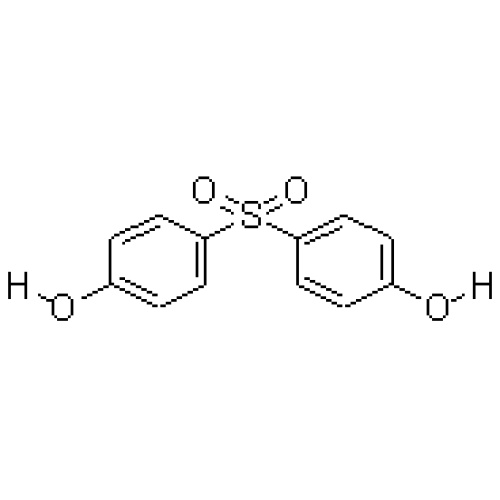

Manufacturers have limited speaking power Bisphenol A is an important phenol derivative, mainly used for the preparation of epoxy resin, polycarbonate and so on. At present, the proportion of polycarbonate used internationally is slightly higher, while domestic production of epoxy resin is the mainstay. In China, there are 4 sets of bisphenol A production equipment. In 2007, the output was about 720,000 tons. The company imported 460,000 tons of bisphenol A throughout the year, of which about 400,000 tons were used for epoxy resin production.

Among the four domestic manufacturers of bisphenol A, Tianjin Shuangfu has ceased production for a long time, and Jianye Chemical Co., Ltd. has failed to put into production at the end of last year. The suppliers are mainly Bayer Shanghai and Wuxi Resin. The two companies have built downstream polycarbonate and epoxy resin devices, and some of them are self-supporting. Under this supply structure, domestic manufacturers have limited voice. Experts said that the market’s recognition of production costs appears to be insufficient. As a result, the market’s stability power is weaker and there are more interference factors. If there is any sign of trouble, it will trigger market fluctuations.

"New Generation" businesses are contending for the competition While manufacturers are hard to dominate the market, market players are contending. As early as 2006, China became the world's largest producer and consumer of epoxy resins. Last year, the output reached 700,000 tons, an increase of 35%. According to reports, about 750 kg of bisphenol A will be consumed for each ton of epoxy resin produced, and the market potential is enormous. Bisphenol A has the characteristics of long storage period, easy transport and storage, and a low operating threshold. Huge demand and convenient business conditions have attracted more and more businesses to join them.

However, some “new generation” businessmen lack understanding of the bisphenol A industry and hope to profit from short-term quick operations. This has a huge negative impact on the market: First, the coordination of the market has become very Difficulty, it is difficult for mainstream merchants to play a leading role. Second, when the market is bullish, they are bought by the wind, the collective low-cost goods are thrown when the market is bearish, causing the overall market to decline. Third, there is no long-term vision and awareness, and it is difficult to bear the responsibility for promoting the sustained and healthy development of the industry. Responsibility and speculation have caused serious damage to the market.

Another reason why the bisphenol A market fluctuates is that the application area is relatively simple. Most of the domestic bisphenol A products are used in the preparation of epoxy resins, but the demand for new materials for polycarbonate has not yet risen, and the pattern of epoxy resin consumption has become extremely large. The simplification of the demand structure is very unfavorable for maintaining the price stability of the domestic BPA market.

In recent years, the domestic epoxy resin industry has continued to develop at a rapid rate. The situation of its two major raw materials, epichlorohydrin and bisphenol A, is quite different. For epichlorohydrin, although domestic production capacity has been surplus, manufacturers have the dominant power, and the imported resources have been basically marginalized. Domestic manufacturers can often increase prices through phased capacity control. Facts have proved that epichlorohydrin has already formed a price-reversal reaction against bisphenol A, that is, when the price of the former increases, the price of the latter declines or stops rising. The upside of the price of bisphenol A is often occupied by epichlorohydrin.

From the analysis of the status quo of the downstream epoxy resin industry, approximately 150,000 tons/year of capacity was put into use at the end of 2007. Currently, the total domestic production capacity has exceeded 1 million tons/year, and there is still room for improvement in the demand for raw materials of bisphenol A. From the end of 2007 to the beginning of 2008, there was also a batch of polycarbonate production capacity in Asia. At present, the domestic BPA industry is facing a new situation, but if we want to overcome the existing bottlenecks, we still need to take various measures. The focus is to increase the level of market intensiveness, expand the fields of demand applications, and gradually increase the supply capacity of domestic resources. Under the premise of increasing supply dominance, healthy and rapid development will be achieved through diversification of consumption.

Jiangxi Hongjiu New Material Technology Co.,Ltd.

Jiangxi Hongjiu New Material Technology Co.,Ltd.